![]()

We are pleased to offer you a complementary sample article from the Dorsey Wright Equity & Market Analysis report of our Technical Research platform. We hope that you find the article insightful and useful. To learn more about the DWA Technical Research platform, click here to take a free 21-day trial. To learn more about Relative Strength and the Dorsey Wright Relative Strength strategies, download the whitepaper Point & Figure Relative Strength Signals. Dorsey Wright & Associates is a Nasdaq Company.

Last week Monday the Nasdaq -100 Index NDX closed at $4,756.04, its highest closing price on record. The record for the highest tick for the index ($4,816.35) still belongs to March 2000, and specifically March 24th, but a new “closing high” has been established this week and this offers both evidence of new demand and also an opportunity to start a few conversations with investor clients. Here are a few topics that might make sense to leverage a notable market event as a chance to educate clients and promote your own expertise.

Surviving Despite Casualties

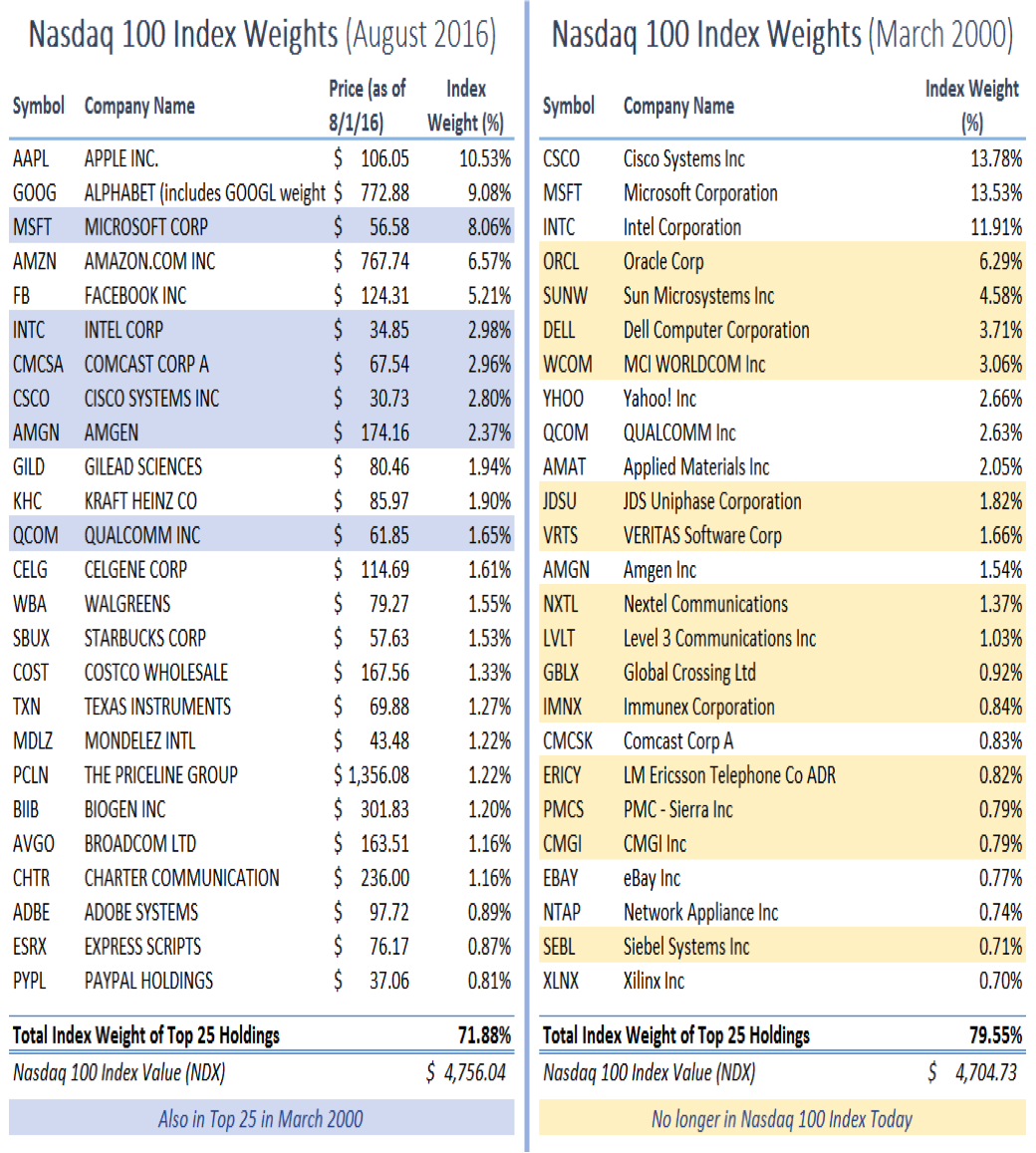

The index construction of the Nasdaq-100 is rather straight-forward, investing in the largest non-financial companies that are listed on the Nasdaq exchange. That list has changed quite a bit more than most would dare to assume over time, and that “changing,” is what allows an index to survive long periods of time despite many of its holdings being unable to do so. An index formed by a market capitalization factor is not expected to be nimble through every market cycle, but the changes that occur over time can be substantial. The process of letting stocks fall out when they lose capitalization helps the index survive by not being stuck with a bunch of securities heading to zero eventually. The image below helps to make this point, as we provide the list of Top 25 weights in the Nasdaq-100 Index today, as well as in March 2000. In both cases, these 25 stocks account for more than 70% of the total index weight. The Index has returned to roughly the same price as it was 16 years ago, but has done so with very different investments. For instance, we’ve highlighted (left) the stocks that are among the Top 25 today and that were also among the Top 25 back in March 2000 (there are only six). We also illustrate (right) how many of the Top 25 holdings in March 2000 are no longer in the Index at all today (the majority of them).

Sector rotation is a byproduct over time for an index of this kind. In the mid-90s the Technology sector accounted for about 1/4th of the weight of the Nasdaq-100, a level of saturation that would rise quite a bit as the index itself did in the 1990s. In a recent article titled, “My How Things Have Changed! A New Look at Nasdaq-100,” Nasdaq discussed some of the changes in complexion this Index has endured over time. “The tech boom of the mid-1990s helped perpetuate the idea that the Nasdaq-100 was a “tech index.” By November 1998, with the tech-driven bull market in full force, technology stocks accounted for an unprecedented 70% of the market cap of the Index. By the early 2000s, tech stocks continued to dominate the Index. Tech continued its prominence into the next decade. Even as recent as 2011, when tech companies were the driving force in the recovery of the financial crisis, technology represented 61.6% of the index market cap.” Today the Index is a little more than 50% weighted in Technology, which is quite a bit beneath its highest such levels, but also twice the Technology exposure observed prior to the 1990s. Leadership can change within a market cap weighted index, it just does so in a different manner and at a different pace. Ultimately, that process allows an index (and the investment products that track it) to have a much higher survival rate than the securities that comprise it.